In Pakistan, the term “Filer” is more than just a bureaucratic label—it is a financial status that dictates how much you pay on almost every major transaction you make. Whether you are buying a dream home, investing in a new car, or simply managing your business finances through a bank, the Federal Board of Revenue (FBR) treats active taxpayers vastly differently from non-taxpayers.

But what exactly is the real, measurable tax difference? In this article, we will break down the withholding tax (WHT) rates applied to individuals on the Active Taxpayer List (ATL) versus non-filers, using real-world examples to illustrate the steep financial penalties of remaining outside the tax net.

What Does It Mean to be a Filer vs. Non-Filer?

Before diving into the numbers, it is crucial to understand the definitions set by the FBR.

- Active Filer: An Active Filer is an individual, Association of Persons (AOP), or company that submits their income tax return by the FBR’s deadline. These individuals are included in the Active Taxpayer List (ATL), which is updated daily by the FBR.

- Late Filer: A taxpayer who submits their return after the due date. While they may still appear on the ATL, they face higher withholding taxes—such as a 6% advance tax on property sales compared to 3% for Active Filers.

- Non-Filer: An individual or entity who is not registered with the FBR or has not filed an income tax return despite being liable to do so. Non-Filers face the highest withholding tax rates and encounter restrictions in financial activities, such as opening bank accounts or applying for loans.

The Withholding Tax Penalty: A Comparative Breakdown

The FBR has designed the tax system to heavily penalize non-compliance. One of the most significant areas where being a non-filer hurts your pocket is in how transactions are taxed. Let’s examine the stark differences in withholding tax (WHT) rates across various categories.

1. Real Estate & Property Transactions

Buying or selling property as a non-filer incurs massive financial penalties.

- Sale of Property: For properties valued up to Rs. 50 million, Active Filers are subject to a 3% tax rate, whereas Non-Filers face a staggering 10% tax rate.

- Purchase of Property: Non-Filers face withholding tax rates of up to 10% on property purchases.

2. Vehicle Purchases and Registration

If you are upgrading your car, being a non-filer will drastically inflate the final price tag.

- Active Filers enjoy reduced rates on vehicle registrations, ranging from Rs. 7,500 to Rs. 250,000 depending on the engine capacity.

- Non-Filers must pay double, with rates ranging from Rs. 15,000 to Rs. 500,000.

3. Banking and Cash Withdrawals

Everyday banking can become a costly affair if you are not on the ATL.

- Cash Withdrawals: For non-filers withdrawing more than Rs. 50,000 in a single day, an advance adjustable tax of 0.6% is deducted.

- Banking Instruments: Purchasing instruments like Pay Orders (PO), Demand Drafts (DD), or Call Deposit Receipts (CDR) also incurs a 0.6% tax for non-filers.

- Foreign Remittances (Incoming): There is no tax for filers on incoming foreign remittances, but non-filers can face a 5% to 10% tax depending on the amount and source.

Summary Table: Filer vs. Non-Filer Tax Rates

Here is a quick reference guide to how tax rates compare for everyday financial and investment activities:

| Transaction Type | Tax Rate for Active Filers | Tax Rate for Non-Filers |

| Sale of Property (Up to Rs. 50M) | 3% | 10% |

| Cash Withdrawal (Over Rs. 50,000/day) | 0% | 0.6% |

| Banking Instruments (PO, DD, CDR) | 0% | 0.6% |

| Profit on Debt (Bank Savings) | 15% | 30% |

| Mutual Funds / REITs | 15% | 30% |

| Independent Power Producers (IPPs) | 7.5% | 15% |

| Dividend Income | 15% | 25% |

(Note: Rates are subject to change based on the latest Finance Act. Always consult a tax professional for the most up-to-date figures.)

Real-World Examples: The Cost of Non-Compliance

To truly understand the impact, let’s look at the mathematical difference in three common scenarios.

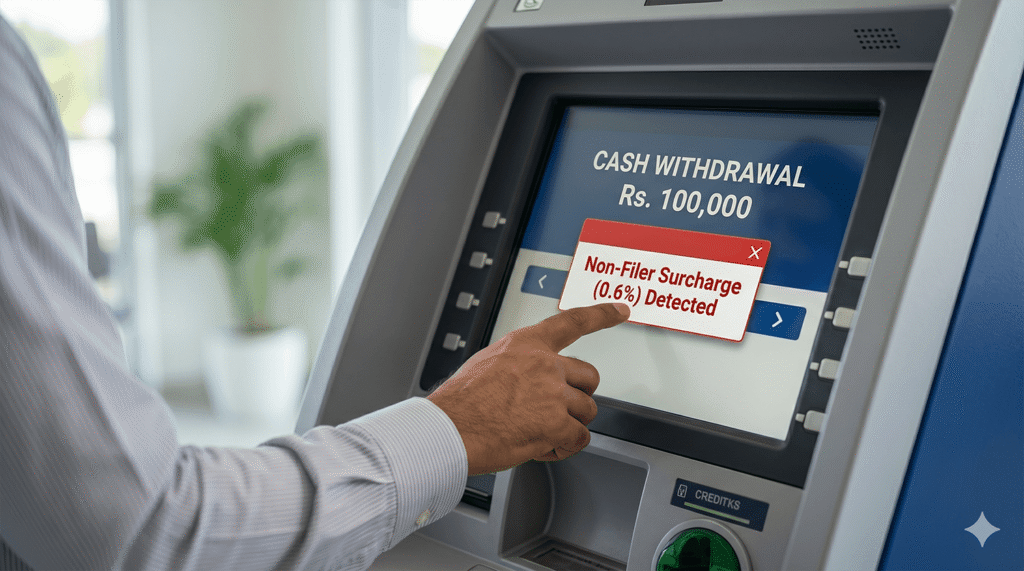

Scenario A: Withdrawing Business Cash

Imagine you run a small trading business and you need to withdraw Rs. 500,000 in cash to pay day laborers.

- As a Filer: You withdraw Rs. 500,000. No tax is deducted.

- As a Non-Filer: The bank applies a 0.6% advance tax because the amount is over Rs. 50,000. You lose Rs. 3,000 instantly just to access your own money.

Scenario B: Earning Bank Profits

You have saved carefully and earned Rs. 200,000 as profit on debt (savings account returns) over the year.

- As a Filer: The withholding tax rate is 15%. You pay Rs. 30,000 in tax.

- As a Non-Filer: The tax rate jumps to 30%. You pay Rs. 60,000 in tax. By simply not filing a return, you lost an extra Rs. 30,000 of your hard-earned savings.

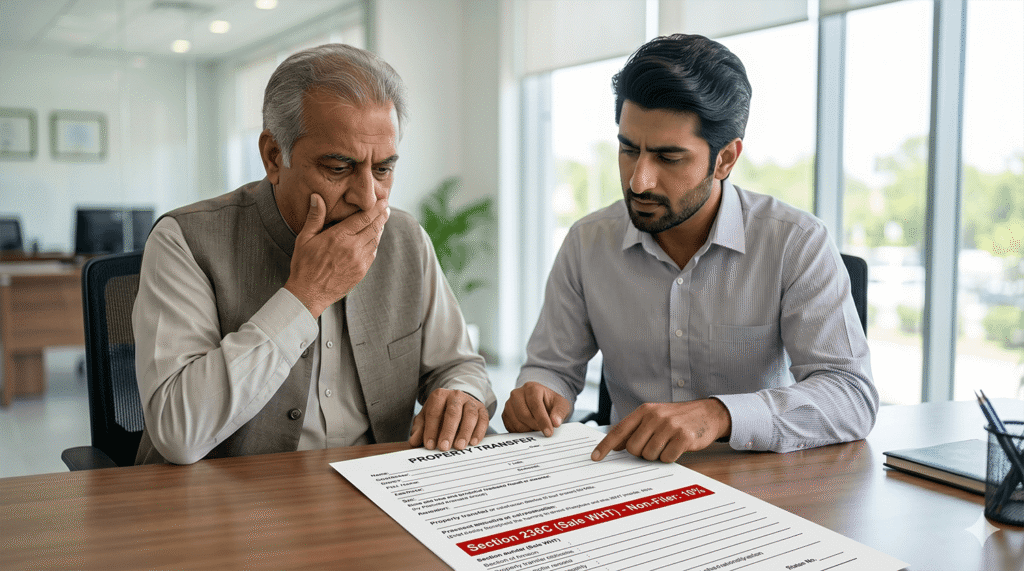

Scenario C: Selling Real Estate

You are selling a family plot valued at Rs. 40,000,000 (4 Crore).

- As a Filer: The withholding tax is 3%. You pay Rs. 1,200,000.

- As a Non-Filer: The withholding tax is a massive 10%. You pay Rs. 4,000,000.

- The Penalty: The non-filer pays an additional Rs. 2.8 Million in taxes alone.

Beyond the Numbers: Restrictions and Credibility

The disadvantages of being a non-filer extend far beyond just higher tax rates. According to current FBR regulations, Active Filers face fewer restrictions when applying for loans, opening bank accounts, or participating in government tenders. Furthermore, maintaining Active Filer status demonstrates adherence to Pakistan’s tax laws, which helps you avoid penalties and enhances your overall financial credibility.

If you are paying advance taxes on your phone bills, electricity bills, or school fees, you can only claim adjustments and reduce your overall tax liability if you are an Active Filer. A non-filer simply loses that money permanently.

Conclusion: It Pays to be Compliant

The numbers do not lie. The Pakistani tax system is heavily structured to reward compliance and aggressively penalize those who stay off the grid. Whether it is a daily bank withdrawal or a once-in-a-lifetime property sale, the “non-filer penalty” can cost you thousands—if not millions—of Rupees.

Becoming an Active Filer is no longer just a civic duty; it is a vital financial strategy to protect your wealth.

Are you tired of paying exorbitant non-filer taxes? Do not let the fear of complex paperwork cost you your hard-earned money. At TaxBRG, our expert consultants can help you register for your NTN, file your returns accurately, and secure your place on the Active Taxpayer List (ATL) quickly and efficiently. Contact us today to start saving!