Opening your email or IRIS portal and finding a notice from the Federal Board of Revenue (FBR) can send your heart racing. For high-net-worth individuals and business owners, an official communication from the tax authorities is often perceived as an immediate crisis. However, receiving a tax notice is not necessarily a sign that you have done something wrong. It may simply be a routine check, a request for information, or a system-generated compliance verification.

In this survival guide, we will walk you through exactly what to do—and what not to do—if you find yourself on the receiving end of a serious regulatory event, such as a notice under Section 122 or Section 176 of the Income Tax Ordinance.

1. Demystifying the Notice: What Does It Mean?

The first step in managing an FBR notice is understanding what the tax authorities are asking for. The FBR typically sends notices through the primary channel of the IRIS Portal, to your registered email address, or via SMS to the mobile number registered with the FBR.

Here are the most common serious notices you might encounter:

- Section 122 (Amendment of Assessment): This is a show-cause notice issued when the Commissioner proposes to amend your tax assessment. Fortunately for taxpayers, proceedings under Section 122 cannot remain pending for an indefinite period of time. A limitation of 120 days has been imposed during which the amendment must be completed subsequent to the issuance of a show-cause notice.

- Section 176 (Notice to Obtain Information): This notice empowers the FBR to obtain specific information. Often, this section is utilized to call for information from a banking company regarding a taxpayer’s financial details.

- Section 111(1) (Unexplained Income or Assets): This is one of the most serious notices. It is issued when the FBR identifies income, property, or assets that you cannot explain from your declared sources. The FBR can treat these unexplained amounts as hidden income, and apply tax, surcharges, and penalties.

- Section 177 (Audit Notice): Issued when your return is selected for a detailed audit, either through a computer ballot based on risk parameters or specific intelligence.

2. Step-by-Step Checklist for Responding

When the notice arrives, a systematic approach is essential. Managing deadlines and gathering facts early ensures that the audit or assessment amendment doesn’t progress aggressively.

Organizing Your Tax Defense

Before jumping into drafting a response, you must establish a timeline and locate your foundational documentation.

- Step 1: Check the Notice Date and Deadline Immediately As soon as you receive the notice, you must identify the response deadline. Deadlines in tax proceedings are strictly enforced. Missing a deadline without requesting an extension is a severe mistake.

- Step 2: Verify the Notice and Identify the Section Identify the section number and the notice type. Log directly into your official FBR IRIS portal to confirm the notice is present in your inbox to ensure it is authentic.

- Step 3: Gather Your Documentation Depending on the section of the notice, you will need substantial proof. For a Section 177 audit notice, you will typically be given 21 to 30 days to submit documents such as financial statements, bank ledgers, contracts, and invoices.

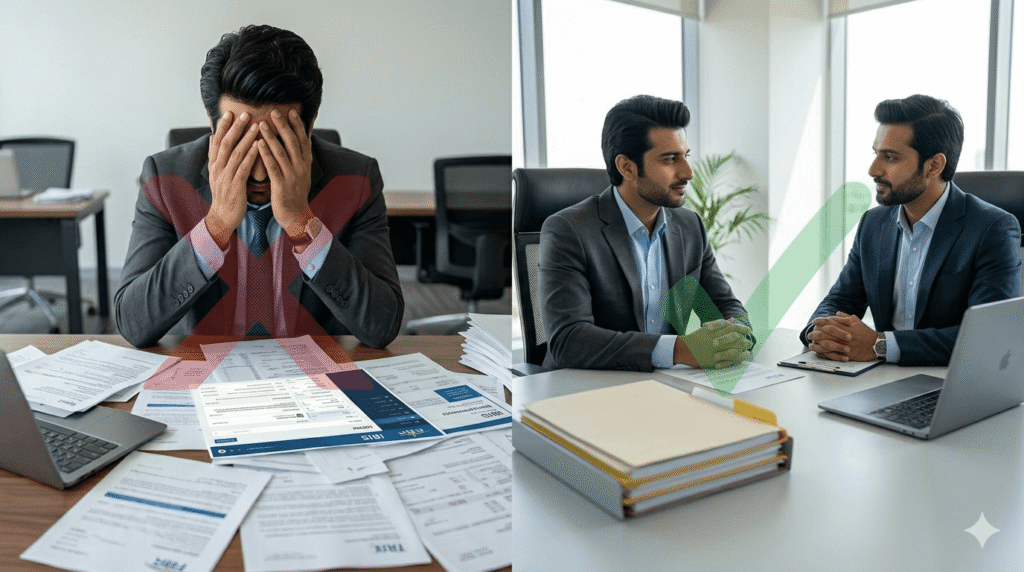

3. What NOT to Do: Maintaining a Focused Mindset

Handling a regulatory event requires a calm, strategic mindset. Panicking can lead to errors that make the dispute far worse.

- Do not ignore the notice: Hoping the notice will simply expire or go away is a dangerous strategy. What you must not do is ignore the notice.

- Do not panic and pay blindly: Never panic and pay an incorrect demand without verifying it.

- Do not respond informally: All communications with the FBR must be on the record. Do not respond verbally or informally.

- Do not admit to unverified errors: Under Section 122 proceedings, taxpayers sometimes admit to discrepancies that a proper review would show were the FBR’s calculation errors rather than their own.

4. The Importance of Professional Representation

Notices issued under Section 111, Section 122, and Section 177 warrant professional advisory support. Responding to a highly technical Section 111 notice regarding unexplained assets is not something you should handle without specialized tax representation.

By engaging an expert, you ensure that your rights as a taxpayer are protected. A qualified corporate consultant will analyze the legal validity of the notice, handle the communication with Inland Revenue Officers, and represent you in required hearings to prevent arbitrary additions to your taxable income.

Conclusion: Take Control with TaxBRG

An FBR notice is a serious regulatory event, but it does not have to be a disaster. By verifying the notice, gathering meticulous documentation, and avoiding hasty admissions, you can navigate the process smoothly.

If you have received an official notice from the FBR, do not face it alone. Engage a tax advisor if the notice is complex. The specialized team at TaxBRG has extensive experience in handling complex tax assessments, audits, and show-cause notices for high-net-worth individuals and corporate clients. Contact us immediately to schedule a consultation and let our experts secure your financial peace of mind.